ADEME's Transitions 2050 scenarios: Focus on industry

In its report titled "Transitions 2050," ADEME examines potential scenarios for following the trajectory of the National Low Carbon Strategy. This comprehensive study across all sectors demonstrates that reducing emissions is still achievable, but it requires drastic decisions. Lemon Energy has analyzed this report and identified key issues for the industry to succeed in this transition.

Industry: The 4th largest source of GHG emissions in France

ADEME defines the industrial sector as "economic activities that involve the production of material goods through the transformation and use of raw materials." "Heavy" industry, in particular, involves the conversion of "natural" raw materials into usable materials. Excluded from this definition of industry are energy production (including refining), civil engineering, and construction.

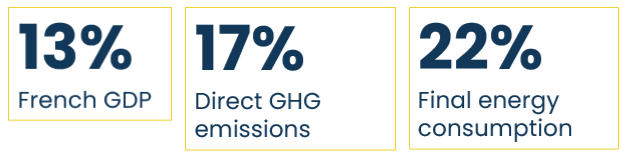

Although the industrial sector accounts for 13% of French GDP, it is responsible for 17% of direct GHG emissions, making it the fourth largest emitting sector. Industry also accounts for 22% of final energy consumption in France, with two-thirds of this consumption attributed to fuel use, primarily for powering furnaces. The remaining one-third corresponds to electrical consumption, mainly for powering motors such as pumps and ventilation.

In addition to GHG emissions, industry has other environmental impacts:

- Material withdrawals, which are linked to the availability of resources.

- Water withdrawals, particularly in chemical, food processing, and paper and cardboard industries, which are comparable to those of irrigation.

- Atmospheric and aquatic discharges of heavy metals, suspended matter, and particles.

- Waste production, with the industrial sector generating 8% (about 26 million metric tons) of the total waste produced in France, but accounting for 25% (2.8 million metric tons) of hazardous waste.

- Soil pollution, with industrial and commercial areas occupying only 0.3% of the French territory, but nearly a third of industrial sites being identified as polluted or potentially polluted in 2015, particularly those engaged in extractive activities.

Unequal impact between heavy industry and other industrial sectors

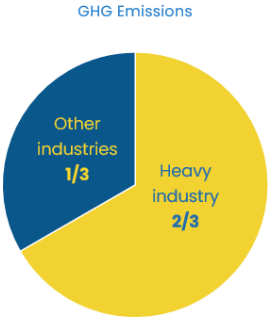

Heavy industry is responsible for two-thirds of industrial GHG emissions. Nine heavy industry sectors have been identified as priorities for decarbonization: steel (steel), cement (clinker and cement), chemical industries (ethylene, ammonia, and chlorine), paper mills (paper and cardboard), sugar, glass, and aluminum production. These sectors share the common characteristic of being energy-intensive, accounting for 60% of industrial energy consumption.

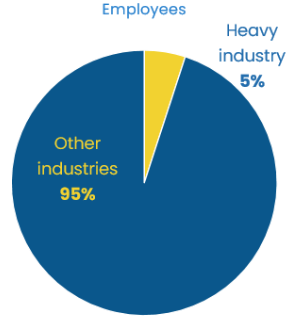

Heavy industry provides a large proportion of inputs for the rest of the industrial sector, which has lower emissions but faces significant socio-economic challenges. Between 2009 and 2019, the number of employees in heavy industry declined by 12.5%, with 140,000 direct jobs in 2019 spread across 1,800 establishments. These salaried employees represent around 5% of the total workforce in the manufacturing industry and 1% of establishments. In contrast, the rest of the industrial sector concentrates 95% of the workforce and 92% of the added value.

Efforts still insufficient

Emissions from the industrial sector have decreased significantly between 1990 and 2018 (-47%), but this decline is largely attributable to regulations on the use of NO2, the decarbonization of the energy mix (replacing petroleum products with natural gas), and economic crises. The importation of products also generates emissions outside of France. The de-industrialization that France experienced between 1995 and 2015 resulted in a decrease in direct emissions within France by 4.5 million metric tons of CO2 equivalent, but this was offset by an increase in imported emissions by 6.8 MCO2eqt.

This decarbonization of industry has slowed down since 2011: -1.3%/year, whereas the SNBC expects -4.6% between 2015 and 2050.

The recent awareness of the carbon cost of transporting raw materials has highlighted the vulnerability of certain sectors to supply difficulties for certain raw materials and/or semi-finished products.

This context makes it possible to consider relocations, i.e. the repatriation of activities previously located abroad, to France. Furthermore, reindustrialization with growth in industrial employment is possible in sectors linked to renewable energies, circular economy activities, or hydrogen production.

Growing pressure from French policy and European regulation

Until now, taxation has been driven by competitiveness considerations rather than decarbonization, and is increasingly affected by energy costs. To move in this direction, France has launched the “Plan de Décarbonation de l'Industrie”.

- At the European level, the European Commission aims to reduce GHG emissions by at least 55% by 2030.

- Within the framework of these regulations, the industry is mobilized:

- Tightening of the ETS directive (carbon quotas)

- Development of carbon taxation

- Integration of the climate and energy constraint in investment and relocation/reindustrialization decisions

- Investment and innovation opportunities for new low-carbon markets

Industrial companies are inclined to implement profound transformations to achieve these objectives.

Structural transformations are needed throughout the industry

The changes will have to be made on multiple axes, in order of priority:

- Adapting to changing production levels. These levels are the main determinants of industrial emissions and are linked to domestic and international demand (and therefore to the sobriety actions implemented). Moreover, the evolution of the food industry is directly linked to the climate issues of agricultural production and to the evolution of diets. For this reason, the territorial industrial network must be efficient and sized according to needs.

- Improve the energy efficiency of technologies and processes to reduce consumption. Each sector has its own specificities, but there are cross-cutting technologies: utilities (chillers, boilers, heat pumps) and recovery of waste heat.

- Reducing the material footprint. The incorporation of recycled material and the modification of inputs towards resources with a reduced environmental footprint imply technical and organizational transformations.

- Change the energy mix in favor of low-carbon energies, particularly to produce heat (steam, hot water) which represents 2/3 of consumption. This modification of the mix includes thermal renewable energies (biomass, geothermal, solar thermal). These transformations place industry in interaction with the energy system.

- Capture, storage and recovery of CO2. CO2 storage remains dependent on the proximity of onshore or offshore capacities, its technical and economic viability and possible local resistance to the installation.

- These necessary transformations are however confronted with multiple obstacles:

- Investment based on short-term profitability and limited by low margins.

- Risk-taking (CAPEX costs, market changes, transformation of production tools, challenges of increasing skills)

- Distrust of citizens (rejection by citizens wishing to maintain their level of consumption, accentuation of inequalities in the face of potential price rises, job losses or transfers, fears linked to environmental pollution).

2050 scenarios

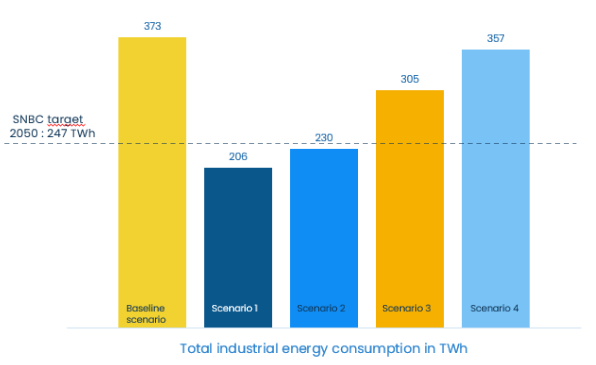

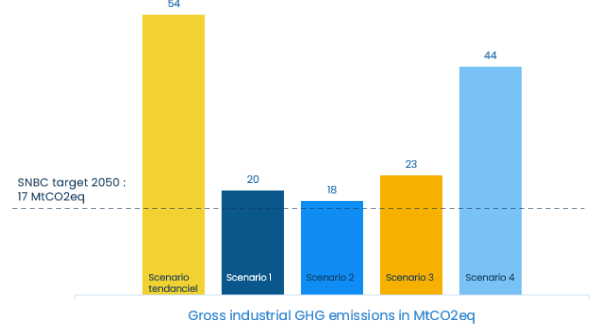

ADEME defines 4 prospective scenarios that would enable us to achieve carbon neutrality in France in 2050. The The comparison of these scenarios with the trend scenario highlights the technical and organizational decisions that must be taken as a matter of urgency in order to comply with the Paris agreements and hope to stabilize the climate below the +2°C threshold.

- Trend scenario: In this scenario, efforts in energy efficiency, material efficiency and the energy mix follow the trend set out in the National Low Carbon Strategy (SNBC). International trade intensifies but is refocused around the EU with the carbon tax at the borders. Production continues to decline, and public authorities continue to support the modernization of industry.

- Scenario 1 Frugal generation: Through strong citizen involvement, production contracts. Protectionism motivated by a concern for sovereignty and the reduction of the environmental footprint generates a transfer of activity towards plant-based agri-foods and recycled materials sectors. These companies invest in energy efficiency to retain market share, green their image, and achieve OPEX savings. B2C companies are imposing more criteria on their suppliers related to the origin and carbon footprint of their products in response to consumer demands.

- Scenario 2 Territorial cooperation: Decentralization and the circular economy are promoted through the strong involvement of local authorities. Re-industrialization and exports are supported by public authorities, with targeted protectionism. Thanks to state support and territorial organization, companies make a major effort on energy efficiency to maintain market share.

- Scenario 3 Green technologies: Institutions focus on decarbonizing the energy mix, with trade concentration in Europe. Energy efficiency prioritizes international competitiveness and electrification. In this context, the government provides Operational Expenditure (OPEX) aid to electrify processes for site modernization.

- Scenario 4 Repairing bet: Companies are urged to innovate and develop CO2 capture and storage technologies, while consumption and globalization intensify. Storage occurs close to sites where feasible, and hydrogen sees significant development.

Overall, the evolution of the energy mix in the scenarios shows a clear decline in industrial consumption of coal, gas, and oil products, in favor of electricity, hydrogen, and, for scenarios 1 and 2, biomass.

Scenarios 1 and 2 succeed in keeping gross GHG emissions within the target of the National Low Carbon Strategy. Scenario 4 could achieve this if the technological challenge of CO2 capture is met.

Levers and conditions for success

Whether driven by consumer frugality or increasingly limited access to material and energy resources, transforming the industrial sector will require significant structural changes.

All sectors will need to reconsider their strategies towards new economic models that are compatible with carbon neutrality: less volume, more added value, more services, and greater reparability of products.

The pressure on a decarbonized energy mix is such that any improvement in the energy or carbon performance of industrial processes must be examined. Therefore, every industrial company must adopt an ambitious low-carbon strategy, with the support of institutions and local authorities.

Support for the low-carbon strategy is provided at several levels:

- Strengthening connections with local areas. The creation of industrial hubs enables the pooling of raw materials, energy, and infrastructure. For example, by recovering waste heat from industrial boilers, it is possible to establish heat networks between industrial players on the same site and/or district heating. This localized circular economy approach also considers non-climatic issues such as biodiversity, water, and soil.

- Directing investment strategies towards new business models and markets for low-carbon products. Institutions actively support this strategic planning and aim to provide visibility and confidence to manufacturers through initiatives such as "Made in France Low Carbon" (France), or "Carbon Contracts for Difference" (European).

- Supporting the evolution of professions by making overlooked jobs more appealing and allowing adaptability between sectors through continuous or initial training. For example, positions such as energy consultant, supported by PROREFEI training, are seeing increased development.

- Respecting a long-term commitment framed by regulations and regular monitoring, to modernize the low-carbon production tool.